FOOD BYTES IS A (ALMOST) MONTHLY BLOG POST OF “NIBBLES” ON ALL THINGS CLIMATE, FOOD, NUTRITION SCIENCE, POLICY, AND CULTURE.

Here in NYC, we are settling into a deep freeze. I sort of like it. The air is a bit more electric and crisper. Clean. Silent. And when the sun shallowly crosses over the landscape and warms you up a tad, you feel so grateful. For those of you, dear readers, who know how this archiver spends her time, I eat a lot of clams (note the header change on the Food Archive). This time of the year has some of the best bivalve eating. This archiver also spends time with her better half making dark and sad music as part of the Sound Furies. It seems that with each passing year, we get less and less snow on the East Coast. It reminds me of this tune we recorded in 2019, but my better half wrote the lyrics when he was young, living in northern California., sleeping in his ‘67 mustang.

last night it snowed though it's almost summer

it hasn't snowed here for 6 yrs

maybe it was the silence, like a blanket in the night

we don't know why we had this dream

Enough pontifications about weather and clams. Let’s get into this month’s Food Bytes. I always like to start the monthly round-up with a few recommended books I have been reading. Here we go. An Immense World by Ed Yong is a fascinating view of how animals perceive the world through their specialized and adaptive senses. Douglas Brinkley’s whopping 600-page read, Silent Spring Revolution, provides a historical deep dive into the beginnings of the environmental movement in the United States in the 1960s. He articulates how presidents and scientists charted a course for protecting the environment (it is my background homework for a book I am working on that I allude to here). This was a time when presidents were presidential (yes, even Tricky Dick is looking good compared to what we are dealing with now…) and worked to preserve the planet instead of watching it all burn. Delano by John Dunne (Joan Didion’s husband) is about the California grape strike led by Cesar Chavez and his sacrifices to ensure that migrant laborers get a fair shake. Again, this book is incredibly timely with the present-day shifts in U.S. “policies” to deport immigrants—the very same people who are keeping us well fed and food secure. And last is Rachel Kurshner’s short story collection, The Hard Crowd. She just oozes cool.

Book reading by the food archiver

Food and cooking

There has been a deluge of articles and media attention on ultra-processed foods. Let’s start with that and then get into real food stories.

The change in attribution of sugar-sweetened beverages to diabetes (T2D) and heart disease (CVD) incidence across regions from 1990 to 2020.

Ah the lovely world of ultra-processed foods (UPFs). These foods are high in sugars, salts, or unhealthy fats and have additional ingredients such as additives, preservatives, and many other hard-to-pronounce ingredients that make them taste good and allow them to sit on shelves for decades. Many scientific articles are trying to attribute UPFs to various deleterious health outcomes, and the evidence, while varying in quality, is building. Enough so that policymakers are taking note. Research suggests that almost 60% of the American diet comprises these foods. Yum. The New Yorker put out an article trying to understand why that is. It is a good read that tries to unpack the evidence. One thing that comes up is that not all scientists agree on the impacts of UPFs on health.

A Nature Food article delves into how governments have responded to regulating UPFs. Most government action has been on consumer education, mainly labeling food products rather than eliminating or regulating the companies that make these foods.

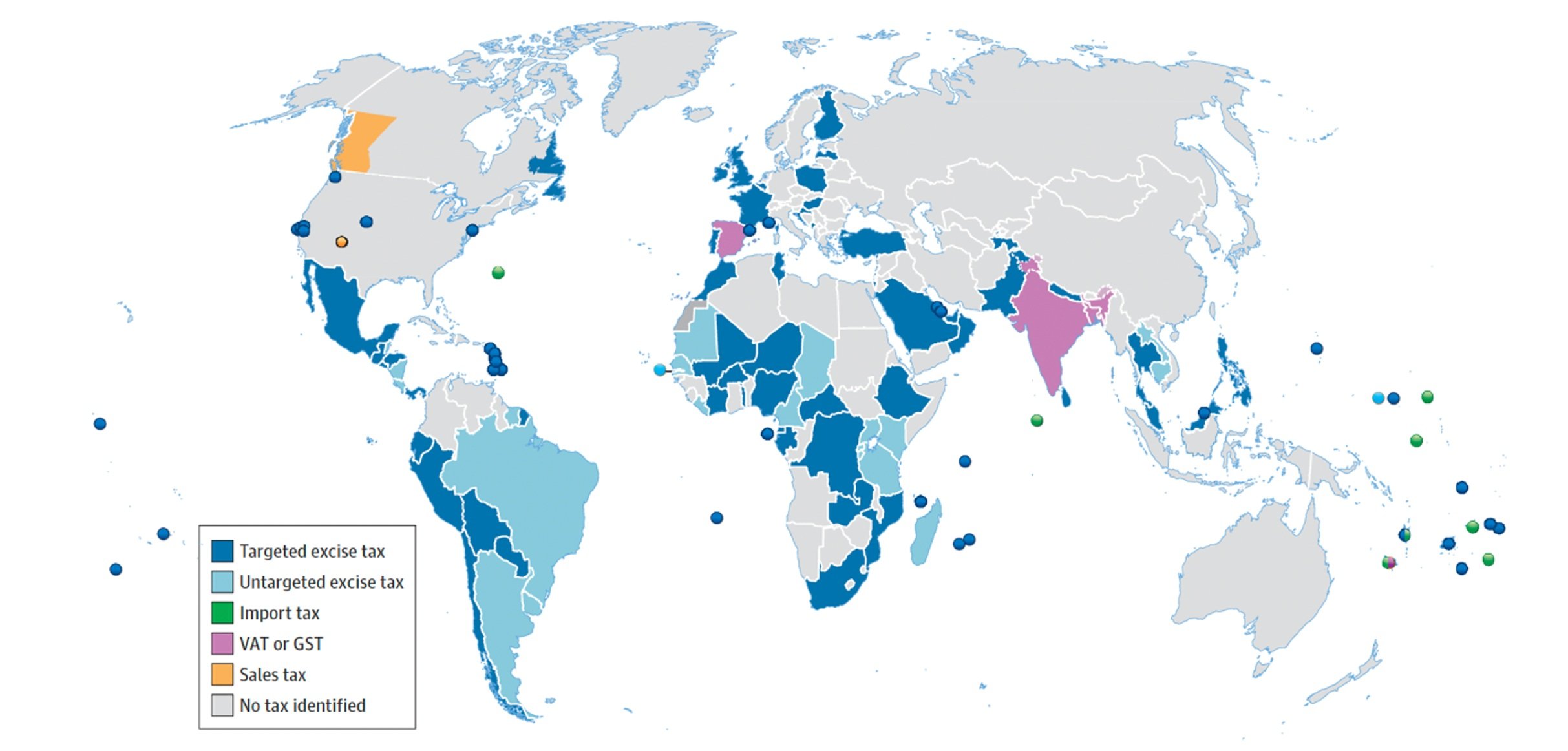

It is not only foods we are talking about. There are also ultra-processed beverages. Using the Global Dietary Database, this Nature Medicine paper shows that in 2020, 2.2 million new diabetes cases and 1.2 million heart disease cases were attributable to sugar-sweetened beverages worldwide. Between 1990 and 2020, the most significant increased attribution of these drinks to diabetes and heart disease was in sub-Saharan Africa! However, sales of these beverages, particularly soda, are rising (see the figure to the right). Great…

Onto real foods. I highly recommend this New Yorker article on the secret history of risotto and the rules that govern how to make this delicious dish whose origins sit on the Po River (a river very constrained by climate change).

Speaking of iconic foods and their origins, those who have lived in NYC for decades likely remember this Indian restaurant enclave in the East Village. You know, the one with all the Christmas lights. Well, in typical warp-speed fashion and the brutal world of restaurant ownership in this city, the Indian restaurant hubs have moved to other parts of Manhattan and, more so, Queens. But still, this one restaurant in the village keeps shining on. Funny enough, my former college roommate lived above this place in the late ‘90s. It is (not)safe to say she had a roach problem.

Then we have tortillas. I wish we had a tortilleria in our hood, but alas, we have to buy the Mission brand tortillas, which taste like cardboard. As this article in the Atlantic suggests, they have lost their magic.

Last, but not squarely in food, the Lancet published a commission to find ways to measure obesity better. With all the kicked-up controversy regarding body mass index as a sufficient measurement tool to delineate overweight and obesity, it’s good timing. Here is a nice infographic that summarizes their recommended diagnostic.

Climate change

Let’s move on to a lighter topic: climate change! In all seriousness, we are in a scary time. This past year, 2024, was the warmest year on record, and the average global temperature was more than 1.5°C above pre-industrial levels for the first time, with 11 months of the year exceeding 1.5°C. To make matters worse, the current U.S. administration has pulled out of the climate accord and plans to “drill baby drill.” This trend and these political decisions fuel our motivation to fight the good fight and ensure the world moves towards mitigation and adaptation solutions, with or without the United States.

The Economist published a well-balanced article on the potential and limits of technology to mitigate climate change through the livestock sector. It is nice to see the International Livestock Research Institute’s work (based in Kenya and Ethiopia) highlighted—who partner with some of the poorest in the world who are tending to animals for their livelihoods.

One issue is to ensure that those countries and populations struggling with undernutrition still have options and choices to consume animal-source foods, particularly in places where access is incredibly and unfairly limited. The Netherlands Working Group on International Nutrition and Clim-Eat put out a brief on animal-source foods in low- and middle-income countries that nicely summarizes the broad evidence. My only gripe is that they should cite the original peer-reviewed publications and evidence toiled over by scientists as opposed to the reports that summarize the said evidence.

Grist, a fantastic climate/environment/food reporting outfit, wrote a worrisome article about how many farmers and farm workers now need to work at night due to extreme heat. conditions Farming is already hard enough, and now this.

Speaking of great journalism, Civil Eats has summarized a set of articles of their “best climate reporting” of 2024. Check it out.

I have lots of time and space for Kyle Davis’s work. In this paper in Science Advances, he and colleagues use high-resolution data on forest cover in Nigeria and find that 25 to 31% of annual forest loss is linked to climate variability. They also find that changes to forest cover have positive associations with dietary diversity, whereas cropland expansion does not. There is much to think about adaptation-wise regarding how the world manages land and forestscapes.

I always have to throw in a critique of the EAT-Lancet Commission. In this paper by Klapp and colleagues published in the Lancet Planetary Health, they articulate a justified framework of shortcomings (see figure below) that the Commission did not address in the first report in 2019 with the hope that these issues will be taken up by the Commission when the 2nd report comes out in the fall of 2025. What I can say at this stage, Anna-Lena, is that we cover some, but not all, of these crucial issues. It looks like a third Commission may be in order!

Current shortfalls of the planetary health diet from a plant-forward perspective by Klapp et al, LPH 2025

Food Systems and Farming

Alignment between food system transformation and degrowth

This paper in Nature Food by Matt Gibson and some of my favorite colleagues Constanza, Daniel, and Mario (yay, Cornell!) presents a fantastic notion that in the political momentum that we must “transform our food systems,” there is also this notion that we have also to consider downscaling of excess production and consumption among high-income countries and overconsuming individuals. The figure to the right shows the alignment (or misalignment) between the goals and objectives of degrowth and food systems transformation.

But some argue that big farms don’t need a lot of transformation and should stay the course of how they are being managed. This article ruffled a lot of feathers. The title, “Sorry, but this the future of farming,” is snarky and reeks of know-it-allism. Anyone who comes to the farming conversation as having THE solution is suspect. This article is the last in the NYT’s series on “What to Eat on a Burning Planet” — a mix of low and high-quality articles with some half-truths. Go to the bottom of this article to see the series.

Let’s get to some farming articles. This paper in Nature Communications argues for the importance of including genomics research and development of what are called underutilized crops, but also called neglected crops or opportunity crops—into breeding strategies, cutting-edge research, capacity building, and representation that some major crops like maize, rice and what get.

A slew of experts published this paper in Nature Food to highlight the importance of small-scale fisheries (SSF). In this mapping exercise, they estimate that SSF provides 40% of the global seafood catch worldwide. This 40% provides roughly 2 billion people with 20% of their dietary intake of six crucial micronutrients. Half of these SSF are women, and many are employed in Asia. Africa supplies the largest catch. This is a fantastic article for those interested in blue foods.

I love this Soil Atlas that comes out each year by the Heinrich Boil Stitlung/EU. This report is chock-full of great case studies and figures arguing for better care and management of soils worldwide to promote resilient agriculture and mitigation of climate change. Called the global silent crisis,” 1/3 of soils are degraded globally, and 40% of those soils reside in Africa.

Self-promotion (sorry!)

I always have to be a bit self-promotional. The Food Systems Countdown Initiative (FSCI) has published its third annual paper in Nature Food and Policy Report. The highlights?

The FSCI interactive tool on the Food Systems Dashboard

Over the past two decades, meaningful progress has been made in improving food systems. Of the 42 indicators examined, slightly fewer than half (20) changed in a desirable direction from 2000 to 2022.

Most of the FSCI tracked food system indicators interact with other indicators, either directly or indirectly, meaning that change in any one area of food systems is likely to affect others and that unlocking change may require coordinated action across multiple dimensions.

Certain indicators related to governance and resilience are key leverage points — and could be critical because of their influence and dependence on other aspects of food systems, and change in them can affect many other indicators.

One cool thing we did was put the indicators and their interactions on the Food Systems Dashboard. You can play with the FSCI data in all kinds of ways. To get yourself oriented, you can find the indicators here, all the data globally and by country, the country profiles of the FSCI data (for example, Kenya), and last, the interaction tool (which is pretty neat).

We’re screwed, but some more than others. And that is not fair…

The scary annual World Risk Report just came out and it just got a bit scarier this year. Gee, I wonder why…we are so screwed.

Reuters published a heartbreaking collection of journalism entitled “Starving World.” Just devastating but worth taking the time to read.

With avian flu sparking and spreading, this article in Nature Reviews Biodiversity is a warning call about pathogens and planetary change.